PART 3: Why won’t economists listen?

Listen to my narrated version here

“We were not trying to start ecological economics. We were trying to influence mainstream economics. But we couldn’t do it, there was no acceptance. So that has led me to accept… that there not only material vested interests from those who benefit from the growth system and don’t want to see it changed, but also intellectual vested interests from economists and thinkers who have invested their time and mental effort into elaborating and studying all these complex models of growth.”

Herman Daly, founder of ecological economics, talking with Nate Hagens in February 2022 (Daly died later that year).

This is the third essay in what I had envisaged as a three-part series, but I have extended to four as I realised I needed more time to explain why mainstream economists seem to so wedded to a particular ideology, and what we can learn from the heterodox economists trying to challenge it. If you don’t know much about heterodox theories and how they compare to the mainstream, I hope this is a useful primer.

This builds on two prior essays: Part 1, on my own 20-or-so years of experience as a mainstream economist, and Part 2, on what I learned from my four-year research effort into why we ignored The Limits to Growth. Part 4: Leverage points for reclaiming economics, is linked below.

I titled this essay Why won’t economist listen? So let’s start with a story about language.

In the Oscar-winning film Arrival, based on Story of your Life by Ted Chiang, the sudden appearance of alien spaceships — positioned seemingly randomly at different points around the globe — triggers a global crisis.

As national defense teams prepare for the possibility of war, the world hangs on one question: why are they here?

Only with the help of a linguist who, at the last hour, deciphers their message, do we learn their true intent.

As it turns out, the placement of the ships was not random. Early in the film, the linguist explains how learning a language rewires one’s brain — we learn not only to speak, but to think differently. The aliens knew their language was so obscure that the countries would have to work together, combining the differences in their own ways of speaking — and thus, thinking — in order to crack the code.

It is a testament to Chiang’s creative genius that he is able to imagine a language that is truly alien. Circular in form, with no apparent beginning or end, it seems to elude time itself. Once learned, it alters the brain, enabling one to see into the future.

The aliens came to offer their language to humanity, to help us to see what is coming — and act accordingly.

But when international co-operation falters, and each country relies on their own narrow interpretations of the aliens’ intentions, a potentially world-ending crisis seems inevitable…

I’d been trying to find an analogy for mainstream economists’ rejection of anyone who questions their theories— even the authors of The Limits to Growth, who came in peace, with a potentially world-saving solution.

My Tipping Point co-creator, dear friend and science fiction aficionado Vegard Beyer suggested Arrival.

The comparison is apt in many ways.

While I was researching the story of The Limits to Growth, I wrote a satirical article in which ecologists and economists meet up every decade from the 1970s to the present day to discuss the state of the world. Each time, they have a diametrically opposite perception of reality. Where one sees rising risks, the other, unbounded opportunities. Where one fears the end of the world, the other cheers never-ending progress.

Renowned chemist and systems scientist Ugo Bardi asked if he could reprint my article in Resilience.org with an opening comment, under the title The Collapse of Rhetoric: Can Economists and Ecologists Talk to Each Other?

Bardi’s commentary encapsulated something I had sensed but hadn’t been able to articulate: ecologists and economists have a completely different language, and thus, way of understanding the world.

Ecologists study the health of ecosystems. Not just the tree but the tree in relation to everything around it — soil, fungi, air, insects, birds, pollution, climate — and all that in relation to each other. This, in turn, requires them to engage with, to listen to other disciplines — much as the linguists in Arrival had to cooperate across borders to learn the alien language. And as the authors of The Limits to Growth did to build their world model.

For reasons I will outline in this essay, economists, by contrast, study the linear correlations, the parts. Like, how GDP relates to emissions, but not how these values in turn relate to others, like food, labour, energy. They also seek to put a monetary value on everything (their “language”), even though many things we value cannot be monetised. Rather than draw on the wisdom of other disciplines, as my sociologist friend (see Part 1) realised, they develop their own set of assumptions about how the world works.

As the countries, acting alone, who suspected the worst of the aliens — this leads to inability to understand what the other side is saying, which sometimes expresses itself (and I’ve experienced some of this) as suspicion concerning others’ motives (“they’re just environmentalists”). Sometimes it emerges as arrogance, derision or even aggression towards those who do not see the world as they do (I’ve experienced this, too).

And it’s not just economists’ positions on climate. As I’ll come to shortly, pretty much all core assumptions of what is typically termed mainstream economics centre not on what is best for our wellbeing, or what might enable our civilisation and other species to thrive for millennia to come — but on the notion of economic efficiency — essentially, extracting as much monetary value from something as possible.

And since it is easiest to take and profit from that which has no voice, which cannot defend itself— nature, undocumented labour, future generations — costs are shoved on to those who are least deserving of the burden, while benefits are funnelled to those who already have so much.

Or, as another Nobel-winning mainstream economist, Angus Deaton, in a remarkably honest reflection, recently put it:

“when efficiency comes with upward wealth redistribution, our recommendations frequently become little more than a license for plunder.”

This leads to several uncomfortable but urgent questions.

If economics teaches theories that are contradicted by reality, by evidence from other disciplines— can economics even call itself a science? Isn’t the basic goal of science the pursuit of knowledge, of truth?

And if the theories — the goal of economic efficiency — at their core undermine societal and ecological wellbeing, ought we be exposing hundreds of thousands, perhaps millions of young people to them each year?

Ought we still listen to economists — if they do not listen to us?

I ended the article cited by Ugo Bardi with a question: who put economists in charge?

That question has been sitting with me since I learned the story of The Limits to Growth. In the next few examples I will try to elaborate on why I think economists won’t listen, and what we can learn from heterodox economists who offer different perspectives. In Part 4 I will bring it together with ideas of where we might go from here.

Around last year’s Beyond Growth conference in Austria, a think tank sponsored by the two leading business lobbies commissioned a group of economists with the task of proving us wrong — that, quite the opposite of needing to rethink our fixation with it, growth was necessary for Austria to become green.

Their logic: like many rich countries, Austria’s emissions have been mildly “decoupling” from GDP for the past few years: that is, the economy has been growing while emissions have fallen. This, they say, is proof it is possible to reduce emissions to zero while continuing to grow ad infinitum.

Up to a point, they have a point. Emissions from Austria’s energy system have dipped in recent years. Some of this was genuine greening: shuttering old coal mines and throwing up wind turbines. But some was just replacing one fossil fuel for another (switching from oil to gas in heating) — or burning more wood, which the EU contentiously classes as carbon neutral. Some, simply from offshoring dirtier practices abroad.

Elsewhere, Austria’s emissions have continued to rise. In land-use, Austria is paving over green spaces (which help suck up carbon) faster than any country in Europe, thanks in part to its love of automobiles (transport is another emissions driver) and single-family homes. Home of the schnitzel, it is also the highest consumer of meat in Europe (an honour it shares with Spain) — another major contributor to global warming.

In short, decoupling to date has barely required Austrians to alter their lifestyles. With emissions still six times the level consistent with “net zero” (if including offshored emissions, even more) — this has to change. Especially as Austria has a goal to become carbon neutral by 2040.

A 2023 report by over 80 climate policy scientists on behalf of the Austrian equivalent of the IPCC concluded that significant structural barriers stand in the way of Austrians being able to live net-zero lifestyles. These range from planning regulations, to “last mile” connections, diets, education and culture.

Many of the experts’ proposed measures align with “sufficiency” measures — such as shorter working weeks, support for the repair sector and expansion of public transport over private travel. In short, measures that may improve life quality, but not necessarily GDP.

“Thus far, living in a climate-friendly way in Austria is

difficult. In most areas of life, from work and housing

to nutrition, mobility and leisure activities, existing structures promote climate-harmful behaviour and make climate-friendly living difficult (high agreement, strong literature base).”

APCC Special Report: Structures for Climate-Friendly Living (C. Görg et al. 2023). English summary here.

But the economists conducting the “green growth” study neglected to cite this work, or indeed, anything but other studies by economists.

Instead, they used the standard econometric tool of linear regression (or, time-series) analysis. They worked out the correlation between GDP and emissions in recent years, and used it to make projections.

Since Austria had already shown some decoupling, the authors concluded that what Austria needed was much faster growth which would lead to even faster decoupling. So they dialled up GDP until they got the rate they needed. Their conclusion: Austria’s economy would have to grow at 7.4% per year in order to achieve net-zero emissions by 2040.

At that rate, the entire economy would double in size within just 17 years.

Let me put this in context. The last time Austria’s GDP grew by more than 7% was in 1971. Today, as a mature economy, growth rarely bounces much above 2%. Only following the Covid lockdowns did growth buck this trend — reaching 5% for two years, followed by two years of recession.

The reason? To grow the GDP you have to produce and consume as much as you did the year before and then some more. To keep growing you need to do that the next year, and the year after, and so on. So you need lots of resources: workers, carers, materials, energy. After the Covid lockdowns there was spare capacity to do that. Now, not so much.

Even if Austria really went all out for growth, it won’t get far in greening without dealing with those structural barriers. Closing down a few ageing coal plants is a different ball game than retrofitting the entire housing stock, connecting 1,000+ rural towns to the rail network or convincing every Oma and Opa to give up their weekly Tafelspitz. Much of that requires, not for-profit, private-sector “solutions” — but public investments in public goods. Not the magic wand of growth, but a whole host of supportive regulations, infrastructure and mind-set shifts.

Even if Austria managed 7.4% GDP growth in any one year, it would certainly trigger an inflation crisis, possibly a recession. That should, really, be basic economic sense. But since the economists’ linear model was not wedded to any physical values — actual resources — and since it excluded feedbacks, it essentially saw no upward limit on growth.

In trying to make the case for private-sector-led growth, if anything, the economists underscored the point of our conference: the climate crisis is not something we can “leave to the market”. And especially as climate is only one of myriad ecological crises we face.

We need to look beyond markets, beyond growth.

And yet, I saw no critique in the media of this well-publicised study. No journalists dissecting their data to expose their clear methodological flaws. Several outlets published the press release verbatim. The usual crowd of conservative commentators cheered it (seemingly, without reading it).

While serious news outlets have long stopped bringing on a climate denier to “balance” the expertise of the climate scientist, some still re-print without question the growth fantasies of mainstream economists — even on issues as serious as how we meet the climate crisis — often without seeking a second opinion.

But then again, it’s hard to find a second opinion when mainstream is the only game in town…

“Monday, 13 April 2015 was a typical day in modern British politics. An Oxford University graduate in philosophy, politics and economics (PPE), Ed Miliband, launched the Labour party’s general election manifesto. It was examined by the BBC’s political editor, Oxford PPE graduate Nick Robinson, by the BBC’s economics editor, Oxford PPE graduate Robert Peston, and by the director of the Institute for Fiscal Studies, Oxford PPE graduate Paul Johnson. It was criticised by the prime minister, Oxford PPE graduate David Cameron. It was defended by the Labour shadow chancellor, Oxford PPE graduate Ed Balls…”

The above is the opening paragraph from “PPE, the degree that rules Britain”, by Andy Bekett, writing in The Guardian, on 23rd February 2017.

Since the Covid crisis many have come to associate PPE with the masks, gloves and Hazmat suits used to keep the pandemic at bay.

But in UK society, PPE has another meaning: it is the acronym for the degree of choice of the budding elite. This list of alumni of Philosophy, Politics and Economics graduates of the University of Oxford reads like a who’s who of former prime ministers, chancellors, broadcasters, newspaper editors and politicians on the left and right.

The three-year degree claims to offer students a rigourous training in the critical and analytical skills needed to grasp the complexities of our modern world.

But it also includes the kind of standard courses in mainstream economics common to most economics degrees around the world. Yet their basis — formally known as neoclassical economics — rather than helping our future leaders grapple with today’s multiple overlapping crises, may instead lead to positions that at best do nothing, at worst, compound our problems.

This is the damning conclusion by a group of leading sustainability scientists, in a widely-cited recent paper in Global Sustainability in which they critically examined ten key hypotheses that form the foundations of neoclassical economics, and four other claims, finding:

“Each fails to satisfy one or more of the basic requirements of scientific practice. Hence, neoclassical economics is fundamentally flawed, is irrational in the common meaning of the word, and should not be used as a guide for government policies.”

If you’ve ever taken classes in economics, some of the main claims may be familiar. They are probably best captured in Harvard professor Gregory Mankiw’s best-selling textbook 10 Principles of Economics. (Fun fact: Mankiw is also a former Bush advisor and multi-millionaire, thanks partly to the eye-watering price tag of his books).

Here are some of the most relevant:

- People are generally self-interested, rational and motivated by money

- Markets are generally the best way to organise our economies, with prices set where supply and demand meet

- Pollution is an externality best dealt with by putting a price on it (like a carbon tax)

- Inflation is caused by government deficits

- GDP, while imperfect, is a useful proxy for prosperity and correlates with wellbeing

Yet rather than generalisations about how our economies work, the sustainability scientists argue they are at best exceptions. By reviewing evidence from social and natural sciences, and even economists’ own studies, they argue:

- People make decisions not on careful weighing of facts but on heuristics, intuition, emotions. We are both selfish and altruistic — we have survived thus far via cooperation, not individualism

- Markets do not work in the way most commonly depicted, where supply and demand magically meet at the price buyers are willing to pay, and suppliers are willing to sell. Indeed one economic study found this foundational textbook example holds in only 10% of cases! Nor can markets provide many of the public goods we need to live sustainability

- Pollution is not external to our economy — our economy is 100% reliant on nature. Returning within planetary boundaries will require more than carbon taxes, which may limit but not halt all harms

- Government deficits are not typically inflationary in countries that issue their own currencies — government spending, such as to deal with resource bottlenecks, can often alleviate inflation

- In rich countries, GDP is no longer correlated with improvements in wellbeing — but it is strongly correlated with energy, resource use and pollution, meaning our economic foundation is actually being eroded as we push for more growth, measured in GDP

While some mainstream economists may grumble that advanced classes offer a more nuanced picture — this is standard fare for introductory courses, which is about all most PPE students will be exposed to. Neither — as was also my experience — do post-graduate courses necessarily come close to the real world. Often, its just more maths. Or, as the authors put it:

“Students are taught invalid concepts at elementary level and more complicated but still invalid concepts, cloaked in difficult mathematics, at advanced levels.”

So if mainstream economics is teaching flawed concepts that the authors say should in no way be used to guide policy — but which today, are still being taught to future decision-makers— can heterodox economics offer a way forward?

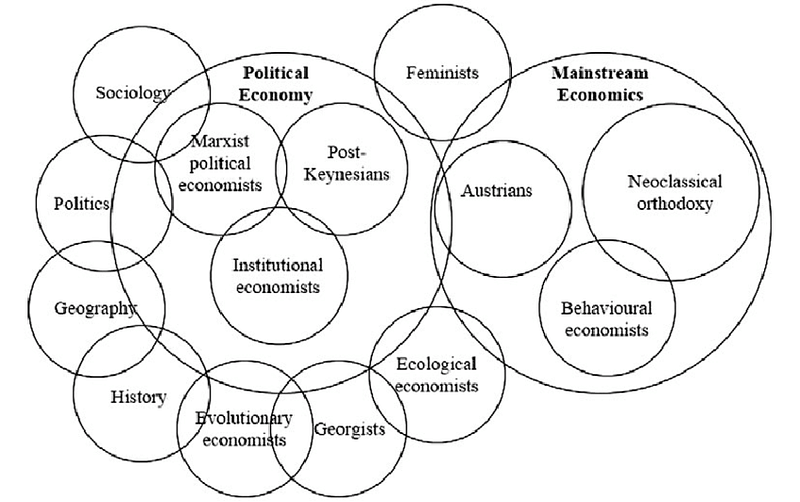

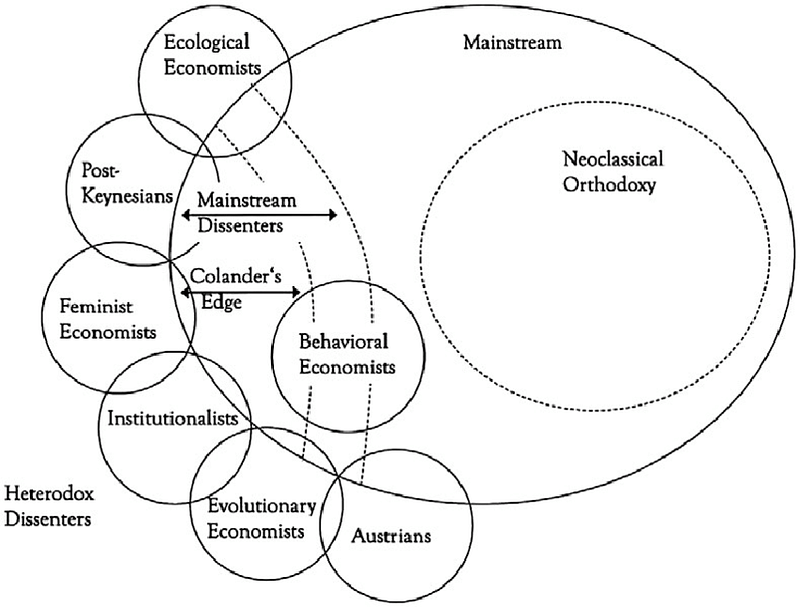

Although the transdisciplinary field of ecological economics focuses directly on achieving planetary and public health and social justice and has grown rapidly since the 1970s, resistance by influential neoclassical economists has ensured that ecological economics, political economy and other ‘heterodox’ approaches to economics have been accepted by only a few Western universities worldwide, have been excluded from prestigious economics journals and have had little public or political impact.

Diesendorf M, Davies G, Wiedmann T, Spangenberg JH, Hail S. Sustainability scientists’ critique of neoclassical economics. Global Sustainability (2024)

In Part 1 I mentioned how the late British Queen had asked an audience of academics of the London School of Economics —in reference to the global financial crash — why did nobody see it coming?

Actually, some heterodox economists did see the financial crash coming. Among them, Steve Keen, a Post-Keynesian economist, who I mentioned in the last article. Keen’s work — and those of his colleagues — in the past decades has not only exposed grave mistakes in mainstream economists’ approach to measuring the costs and risks of climate change, but in our understanding of money, which, as I’ll explain, undergirds some of the core arguments about the need to grow.

But before I get to that — what is heterodox economics?

Broadly speaking, economics falls into two camps: the mainstream/orthodox camp and the much smaller heterodox one. Data are scarce, but my rough calculations (based on courses listed on the websites of their associations) suggest less than 1% of undergraduate degrees and well under 10% of post-graduate ones are heterodox.

While the mainstream sees the economy as governed by market forces, heterodox economics, part of the broader field of political economy, views the economy as shaped by shaped by political and natural forces. As such, they tend to work in a more interdisciplinary way, combining insights from other social and natural sciences.

However, drawing a hard line between fields is not always easy. As challenges to its core principles have emerged over the years, the mainstream has had a tendency to co-opt the bits that align with its preference for markets and growth — and quietly discard the rest.

Such has been the case for behavioural economics, which evolved to reconcile the mainstream assumption that people are rational with decades of behavioural science to the contrary. The result, though, is that it is often used to maintain the status quo, to nudge rather than address the root causes of our problems. As such, behavioural economics is broadly viewed as a mainstream discipline.

Even development economics, which was the subject that first opened my eyes to orthodox critiques (see Part 1), appears to have been subsumed into the mainstream in recent years.

Then we have divisions of over how mainstream economists — versus heterodox — treat the environment. Herman Daly, a contemporary of the authors of The Limits to Growth, who I cited at the top, was a World Bank economist and founder of ecological economics, a heterodox field.

However, as he explained in one of his last interviews before his death in late 2022, Daly didn’t set out to create a new field — but to attempt to improve mainstream models, by integrating nature.

But because his models pointed out that our earth is finite, he concluded we’d eventually need to transition to an economy beyond growth — a steady state, where we learn to prosper within earth’s limits. As with the The Limits to Growth, the mainstream rejected his proposals.

Today, the discipline of ecological economics is most closely associated with post- or degrowth research. And it is among the least-studied of all heterodox fields. The authors of the above article counted just ten degrees in ecological economics, out of literally thousands worldwide. And only one was an undergraduate degree, meaning there are almost no options available to young people who wish to understand ways we might manage our economies without growth. Even though, on our current trajectory, that is the most likely outcome.

Moreover, not one of the programmes is offered by the ivy league, the training ground of our elite. Oxford PPE students, if they care to pick it from among a dozen electives, can study the mainstream version of environmental economics a la Nordhaus (see Part 2) — which rejects limits to growth and aims to solve our most urgent problems through the market.

The example of PPE shows how, within mainstream economics, climate remains a niche issue. Not just externalised in models but in economic departments and in academic journals where, at least until recently, the top journal had featured not one article on global warming. Across the top ten, there were three times as many on baseball and basketball as arguably our most urgent crisis.

As I’ll come to in Part 4 — the unwritten rule that one must publish in a leading journal is partly what maintains the cognitive dissonance. Budding scholars are discouraged from picking such “passion” topics as climate and focusing on subjects that will get them a job at a leading institution. You know, like ball sports.

Even William Nordhaus claims he couldn’t get his earlier papers published in mainstream journals. That he was essentially left to get on with developing his own is version of climate economics for so long greatly explains why we are where we are.

By this token, one might excuse environmental economists as doing their best in a discipline that teaches climate complacency (including to many of our future leaders). As I’ll argue next time — it helps explain, but — given the severe failings of their models — it does not excuse their dismissal of heterodox fields like ecological economics.

I should point out here: not all heterodox economists are critical of the growth paradigm, though they do tend to be more critical of capitalism — as understood as a system centred around the pursuit of profit (rather than some greater purpose), the protection of private property (versus public or collective ownership) and competition (versus cooperation).

Feminist economists are some of capitalism’s harshest critics. They emphasise how our entire economy is upheld by the unpaid work of creating and caring for a labour force without which no growth would be possible, but which — like nature — is completely discounted from mainstream models. This is why they tend to favour policies to reduce working hours (helping share the care burden) and value professional care.

Then there are the Post-Keynesians, like Keen, who emphasise the importance of institutions, and an active state to tame markets’ animal spirits.

So now we come to Keen and his contemporaries’ contributions to countering the prevailing wisdom that our economies must grow.

It’s all about money. Or rather, debt.

In mainstream models, money is viewed as a medium of exchange.

The story goes something like this. People work for money, which they use to buy what they need, depositing the rest in banks or investing in other assets. The banks take this money and lend it out to companies, which generate all the goods and services in our economy. Governments take a portion in taxes to pay for the things markets cannot (fully) provide, like roads, street-lighting and primary education. If governments spend more than they “earn” in taxes, they create deficits which — according to mainstreamers like Mankiw — cause inflation and crises.

As Keen and a sub-group of Post-Keynesian economists who developed Modern Monetary Theory (MMT) have pointed out — this whole story is factually incorrect (even the Bank of England knows this).

Money does not magically appear from the market — it is created, by governments and by private banks (who are licensed by governments) when they create loans. It is, ultimately, debt. (Actually, an important contributor to this theory was not an economist at all, but the late, great anthropologist David Graeber).

This means governments with their own currencies (such as the large G12 economies) cannot go bankrupt (there actually is a magic money tree). Neither are deficits inflationary, as long as the resources — the workers, the materials — are available. Or as British economist John Maynard Keynes, back in 1942, said:

“Anything we can actually do, we can afford”

By contrast, when governments try to keep their budgets in surplus, to grow the economy — since all growth requires money — the private sector must step in.

As MMT economist Stephanie Kelton has pointed out, it has been risk-taking by private banks (often driven by lax regulations) that has fuelled every one of our economic crises this century except for Covid, and it has been government austerity — attempts to reduce deficits — that has prolonged or deepened crises, driving inequality, cuts to climate spending and, some studies suggest, bolstering the far right.

That is, most crises have emerged not from governments' over-spending, but from private banks’ risky lending. And they have emerged from within the system. So economists really ought to have seen them coming, and even if they could not stopped them, they could have certainly lessened the fall-out by siding not with the banks but with ordinary people (some economists did, but not the ones advising our leaders — more on that next essay).

Understanding the money — or deficit myth, as Kelton calls it — is one of the key ways in which have become locked in the growth paradigm — and it is perpetuated by flawed mainstream theories.

And it helps explain why Oxford PPE graduate and Labour Chancellor Rachel Reeves is currently tearing up the remains of the welfare state — in the name of slashing the budget deficit — while relaxing rules for billionaires. Why her government is investing billions in expensive carbon capture and expanding airports to “boost growth” — but still failing to put up the funds to retrofit Britain’s leaky homes.

But, flipped around — this also means we do not need to wait for growth to fix our problems. We do not need the taxes of the wealthy (though we ought to tax the wealthy, as they consume too many resources). We do not need private equity firms to buy up our public services so that governments can “free up” their meagre budgets for climate investments (and only investments that maintain business-as-usual, mind, nothing that might improve broader wellbeing).

It is possible to envisage an economic system centred on sufficiency, where public money is used to mobilise resources where we need them — not simply to where it can make the most profit. Where human needs, especially in the over-consuming Global North, are fulfilled at far lower levels of energy and material use — because products last longer and because we are not manipulated into consuming by ads and algorithms. And where innovation is targeted towards meeting our needs while repairing and supporting our life-giving planet — not the vague goal of more growth.

We do not need to wait for growth to solve our problems. Indeed, we urgently need to have a broad debate about needs to grow — and what needs to shrink, and how we might feasibly transition to an economy beyond growth.

And that debate — right now, is not happening. Mainstream economists are not listening. And heterodox economists are not being given a voice.

And that is because economics has been captured.

If you find this essay useful, you can support my project to turn it into a documentary series → here.